Trillions of blue ocean market, the hydrogen

1.1 hydrogen is an ideal alternative to fossil fuel energy

Hydrogen rich resources, and accessible, with sustainable development. Hydrogen is more content elements in the universe, the earth all elements reserves is third, and so the resources has the adequacy of energy supply. Second, most of the hydrogen in the form of water exists in the nature, raw material is easy to obtain. In addition, as early as in 1970, general motors is put forward the concept of "hydrogen economy", its core is to use the chemical property of the hydrogen recycle. Hydrogen production from water by water and oxygen reaction releasing chemical energy, and after use of the product is still water. No other intermediate throughout the whole process, no waste, zero pollution. Thus forming a recycled closed loop system, sustainability has great advantage. "Carbon neutral, carbon peak" in China's big background, the commercialization of hydrogen utilization has become the hot spot in the market.

Hydrogen gas calorific value is high, it is existing the ideal alternative to fossil fuel. According to the chemical properties of hydrogen, we found the common fuel heat value is high (142 kj/g), is about three times as much as oil, coal of 4.5 times. This means that if the consumption is the same quality all kinds of fuel, hydrogen energy is provided by the big one. The characteristics of high heat value will play an important role in traffic tools to implement and lightweight.

1.2 complex hydrogen industry chain in China, the theory of economic value

The hydrogen production chain into hydrogen production, storage and transportation, filling stations, many links such as application of hydrogen fuel cells. Hydrogen production chain is longer than the lithium battery industry chain, complexity, higher content of theory of economic value. The hydrogen in its industrial chain, and policy support is particularly important, under the policy support industry into the "scale - authors - develops the market" the amount of the price cycle. In addition, the ongoing technological progress would be feedback to solve the core technology of each link cost restriction, step into a commercial competitiveness.

Hydrogen 01. Hydrogen production: the "grey" to "green" hydrogen development, large-scale low-cost is the development direction

In order to distinguish the purity of the hydrogen production way (carbon emissions), we will get the hydrogen renewable energy electrolysis of water known as the "green" hydrogen, including renewable energy hydrogen and the hydrogen production by electrolysis of water and so on, the core characteristics for the production process can achieve zero carbon emissions. Hydrogen "grey" refers to the fossil energy as the raw material, through steam reforming of methane or autothermal reforming methods such as manufacture of hydrogen, although the cost is low, but higher carbon intensity. Hydrogen hydrogen cleanliness is between the "green" and "grey" is "blue hydrogen", its core technology is in the process of production increased carbon capture and storage (CCS) links, reduces the carbon emissions in the process of production, but you can't eliminate all carbon, is a relatively modest way of hydrogen production.

Our pv wind power installed peak, electrolysis of water hydrogen production prospects. Photovoltaic leading longji shares into pv hydrogen production, is our country the overall development of the photovoltaic industry to explore water electrolysis hydrogen production landmark step on the road. Because the electricity of the total water electrolysis hydrogen production cost of about 80%, so the cost of water electrolysis hydrogen production is the key to energy dissipation problem. On the one hand, by developing a PEM and SOEC technology can reduce the energy consumption in the process of electrolysis, on the other hand depends on the development of photovoltaic (pv) and wind power low cost hydrogen production. According to figures from the National Energy Administration, 2020 for the 71.67 million mw wind power and solar power 48.2 million kw, scenery of the new power and about 120 million kilowatts. According to its Chinese energy research institute, photovoltaic (pv) system in China in 2019 KWH cost about 0.29-0.80 yuan per KWH, to 2025 annual electricity cost in 0.22 0.462 yuan per KWH. Onshore wind KWH cost about 0.315-0.565 yuan per KWH, and falling in the future there is still a certain space, is expected to 2025 annual electricity cost in 0.245 0.512 yuan per KWH.

Industrial by-product hydrogen hydrogen production technology mature, low cost, is expected to become an important source of the recent high purity hydrogen. Industrial by-product hydrogen hydrogen production refers to the use of hydrogen industrial exhaust gas as the raw material of hydrogen production mode of production, including coke oven gas, alkali by-product gas, refinery dry gas, synthesis of methanol and ammonia, etc., use efficiency is low, had a higher proportion of surplus. Industrial by-product hydrogen resources are rich in our country, which represented by the kam energy of coking enterprises is using coke oven gas to hydrogen making ash, industrial by-product hydrogen is the short term for economically feasible ways of hydrogen production.

02. Hydrogen storage: high pressure gaseous hydrogen storage has been widely used in liquid and solid hydrogen storage was still in the stage of research and demonstration

As hydrogen from production to use the bridge, in the process of hydrogen storage technology is the core of the hydrogen energy, in the form of stable, stored for subsequent use. Hydrogen storage is mainly divided into three ways, including gaseous hydrogen, liquid hydrogen storage and solid hydrogen storage. In domestic high pressure gaseous hydrogen storage applications are widely at present, the low temperature liquid hydrogen storage in the aerospace and other fields to the application of organic liquid hydrogen storage and solid state hydrogen storage was still in the stage of demonstration. At present domestic main cryogenic co, rich rhett, installed, the capital stock, sinoma science and technology companies such as the hydrogen storage layout.

03. Transporting hydrogen: with long tube trailer transport high pressure gaseous hydrogen is given priority to, the future after the scale to the long-term development of networks

Hydrogen transport according to its shape can be divided into gas transportation, liquid and solid transport, including gas and liquid flow is the main mode of transportation. Hydrogen transport now is given priority to with high pressure gas transportation short-term long tube trailer, but the pressure and the capacity remains to be improved; Liquid hydrogen transport is widely used in foreign mature technology region, our country has not yet reached the level of civil.

According to hydrogen cloud chain contrast analysis of the hydrogen gas pipeline and gas pipelines, on a hydrogen pipe construction situation, standard, material selection, design and manufacture, the accident consequence and there is a lot of progress on security spacing space:

(1) the construction status quo: compared to natural gas pipeline, less amount of hydrogen gas pipeline construction, pipeline diameter and design pressure is low, the relevant standard system is still not perfect, the current domestic long distance gas transmission pipeline is still not suitable for the hydrogen design standard, should focus on strengthening the standardization of long-distance hydrogen pipeline technology work.

(2) standard: because of the influence of the environmental hydrogen embrittlement, hydrogen gas pipe material is more strict restrictions, material with high pressure hydrogen environmental compatibility test requirements, ASMEB31.12-2014 recommended X42, X52 pipeline steel such as low intensity, and must consider the problem such as low temperature shift performance.

(3) selection of materials: in order to reduce the probability that the hydrogen induced failure occurred, compared to natural gas pipeline, the design formula in hydrogen pipes added "material performance coefficient", improve the level of the whole wall thickness of the pipes, at the same time the hydrogen pipe butt welding preheating before and after welding heat treatment requirements more stringent.

(4) design and manufacturing: compared with gas leakage, pipeline in high pressure hydrogen leakage of dangerous clouds and larger set, the spread of highly increase faster, smaller in the surface area of dangerous consequences, but hydrogen influence range, are more likely to spread, and achieve the same flame thermal radiation levels, the hydrogen gas heat distance closer, energy is relatively stronger.

(5) the accident consequences: small hydrogen gas pipelines buried thickness and gas pipeline difference is small, but the hydrogen pipe with small spacing between underground pipes and other buildings require significantly higher than the natural gas pipeline, so in order to avoid high-pressure hydrogen leak happened after the trigger a domino effect.

Hydrogen gas pipeline construction in China is still in its infancy. By 2019, the United States has about 2600 kilometers of a hydrogen pipes, Europe has 1598 kilometers, and the hydrogen gas pipeline in our country, still stays at the level of "hundreds of kilometers", a total of about 400 km, mainly distributed in bohai bay, Yangtze river delta and other places, is located in luoyang, henan jiyuan and hydrogen gas pipeline is the current mileage between long, large diameter, high pressure, hydrogen gas pipelines, bue to its pipeline mileage is 25 km, the pipe diameter of 508 mm, a hydrogen pressure of 4 mpa, NianShu hydrogen volume reached 100400 tons. According to "China blue hydrogen infrastructure development is expected, by 2030, the hydrogen gas pipeline in our country will reach 3000 km.

04. Hydrogenation: core equipment imports, domestic open step by step

Filling stations of technical route is mainly divided into integrity hydrogen technology and technology for hydrogen, hydrogen filling stations of China source comes from the most points for high-pressure hydrogen. According to OFweek statistics, the current domestic operating filling stations, the only source of dalian new hydrogenation station, Beijing yongfeng filling stations have the ability to stand integrity of hydrogen and the rest of the hydrogen gas mainly comes from external for hydrogen filling stations, using hydrogen long tube trailer (transportation of high pressure gaseous hydrogen, liquid hydrogen tank lorry (transport cryogenic liquid hydrogen filling stations and back and forth between hydrogen source. Integrity of hydrogen technology, including natural gas reforming hydrogen and water electrolysis hydrogen production. Among them, the electrolysis of water hydrogen has the wide application and technology has been very mature, for use by most of the European filling stations.

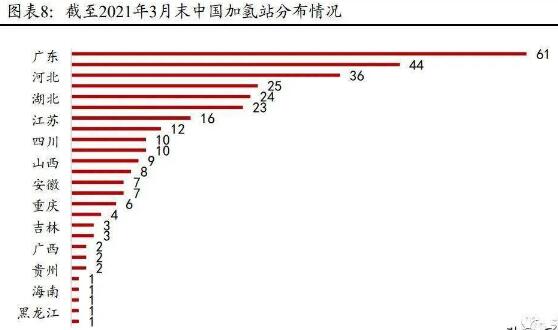

Guangdong, hebei province, hubei's top three, large filling stations are still scarce. According to GGII incomplete statistics, as of December 31, 2020, the national construction and has built 181 filling stations, has been built for 124, including a total of 2020 completed filling stations 55. Built in 2020 in domestic 124 filling stations, 105 with clear filling ability. And further analysis the 105 filling stations, most for hydrogenation capacity of 500 kg/d (12 h) filling stations, a total of 50, accounted for 47.26%; 1000 kg/d (12 h) of filling stations have 20 seats, accounted for 19.05%, hydrogenation capacity more than 1000 kg/d (12 h) there are only 7 of hydrogen stations, accounted for 6.67%. As of March 2021, a high number of filling stations layout in China in the first three known as guangdong, hebei and hubei, the quantity of 61/44/36 respectively.

From the perspective of the function of hydrogen station, domestic & stand proportion increase year by year. According to the filling station specification (gb GB50516-2010), single filling stations can station construction, but the disadvantages need to location and high input costs and construction of composite filling station can reduce operational costs. Domestic is currently actively explore "oil, hydrogen, gas and electricity" joint construction operation mode, petrochina, sinopec and other state has embarked on the related research and development and construction.

05. Fuel cells: into the early stage of industrialization, has a broad development prospects

National energy group, sinopec, petrochina and so on more than 20 large state are hydrogen crossover development industry. By the end of 2020, China's fuel cell car ownership 7352 vehicles, fuel cell vehicles in our country has entered the early commercialization.

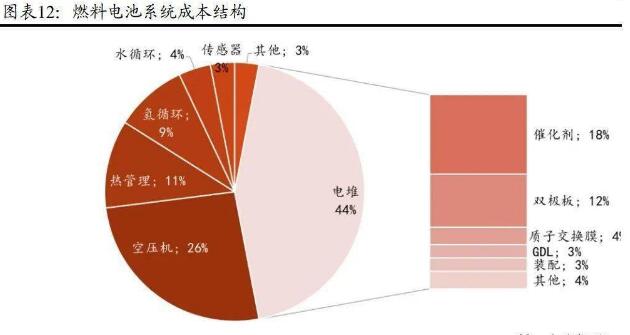

Pile occupy half of the fuel cell system cost, localization still exist. According to the calculation of the U.S. department of energy (doe), the system is the core part of the cost of fuel cell electric shocks, air compressor. Cost estimates of 80 kw system, under the condition of the annual output of 500000 sets of large-scale, pile occupies 44% of the cost of fuel cell system, and the air compressor accounted for more than a quarter. Pile and the air compressor is the key to reduce the comprehensive cost of the fuel cell system. Proton exchange membrane, catalyst, membrane electrode core components such as unrealized localization, the production efficiency is low, cost is high, is still a core problem in the development of fuel cell.

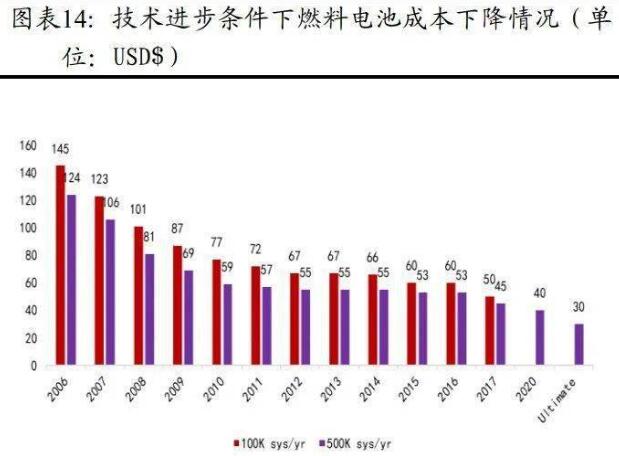

Fuel cell system basic performance meet the requirements, cost reduction is the focus of the future. Comparison of the energy saving and new energy vehicle technology roadmap (2016) put forward the technical target, at present our country passenger cars and commercial vehicles with a fuel cell research and development and performance of the system has meet the requirements, but the cost from its target requirements still have very big difference, still is made about the commercialization of fuel cell vehicles. According to the U.S. department of energy (doe) estimate of the cost of fuel cell vehicles, expansion of the scale of production will lead to the cost of the fuel cell system will drop significantly. Based on the technical level of 2020, the annual output of 500000 sets of 80 kW electric pile under the scale of proton exchange membrane fuel cell system cost can be reduced to $40 / kW, 80 kW fuel cell car battery system valued at about $3200 (20000 yuan).

2 way resistance and row is around the corner, the hydrogen challenges and opportunities in China

2.1 the top design gradually clear, make clear further fuel cell commercialization path

National energy bureau released the energy law (draft) "to the hydrogen to coal, oil, natural gas is classified as energy and conventional energy sources such as wind power. 12020 month, in the new era of China's energy development, "the white paper points out that the development and utilization of the fossil fuels is the main way to promote green low carbon energy transformation. Future will speed up the green industrial chain of hydrogen production, storage and application of hydrogen technology and equipment development, promote the hydrogen fuel cell technique and the development of hydrogen fuel cell car industry chain. Will hydrogen and energy storage as a "difference" plan for the future industry forward planning, from the national strategic leading the hydrogen industry development in the future. Promulgated by the State Council and of the new energy automobile development plan (2021-2035) and automotive engineering society of China published "energy conservation and new energy vehicle technology roadmap (version 2.0) is more for our country the hydrogen development put forward more specific requirements and guidelines. As the country "carbon neutral", "carbon peak" task, the hydrogen this green energy brought to the attention of the countries and push. The above-mentioned documents, for hydrogen "system", "store", "yun", "add", "use" are the layout of each link. Core of positive plate including scenery water electrolysis hydrogen production, filling stations and other infrastructure construction, hydrogen fuel cell vehicles, etc.

The Treasury five ministries and commissions such as joint mandate, of "replace subsidies with awards" promoting the development of hydrogen fuel cell vehicles. The notice about conduct fuel-cell vehicle demonstration application rules of fuel cell car demonstration goal and integral evaluation system of urban agglomerations in two aspects: in the field of fuel cell car application, the key indicators of evaluation are applied vehicle technology and quantity; In the field of the hydrogen supply, the key indicators of assessment for the hydrogen supply and economy. Policy of "replace subsidies with awards" demonstration core: take medium-duty commercial vehicles, urban agglomeration as the lead, strengthening strong chain, chain of fuel cell industry chain. Under the subsidy policy, the application of fuel cell car floor mainly for car companies, the "notice" will be to demonstrate the core tasks for the development of urban agglomeration. "Notice" also points out that the demonstration of urban agglomerations can also get more reward, after the demonstration overfulfilled task overfulfilled part of bonus. All this policy has greatly inspired the various provinces and cities on the development of hydrogen energy industry and to the application for the force of the demonstration of urban agglomeration. Hydrogen fuel-cell vehicle demonstration city group policy is released, there are nearly 20 urban agglomeration declare hydrogen fuel-cell vehicle demonstration, domestic more hydrogen thermal electricity industry development. As the group released the list of future demonstration city, the development of the hydrogen industry will to the next level.

2.2 where the hydrogen release policy one after another, the provincial government of hydrogen industry enthusiasm

Is guided by the state general direction, as well as of "replace subsidies with awards" and other relevant incentive policy, local governments have also responded to an appeal by the state and by the hydrogen policy guidance. With a quarter of 2021, many local governments have for the next few years the hydrogen industry development put forward specific planning.

2.3 China's emission reduction task, double carbon promises to bring opportunities for hydrogen energy development

According to China's commitment to the 2030 and 2060, will achieve "carbon peak" and "carbon neutral" the grand goal. For now, however, China's arduous task of emission reduction. According to the UN "Emission Gap Report 2020" data, China's carbon emissions about 14 billion tons in 2019, from the total accounted for more than a quarter of the total global emissions, is still the world's top emitters. In response to global climate change, the performance of the carbon reduction target in the Paris agreement, according to the national renewable energy center, established the energy policy in China still needs to reduce fossil fuel use of ratios to achieve the target of climate change is lower than 2 ℃. Build clean, therefore, low carbon, safe and efficient modern energy system is imminent.

Hydrogen electric coupling is an important approach to build our modern energy system. At present, China's energy development gradually from the weight of the expansion to mention mass efficiency, energy efficiency, energy structure, energy security has become our country energy three key to the development of the high quality. Compared with other transformation methods, combining hydrogen and electricity will become the important way of modern energy system.

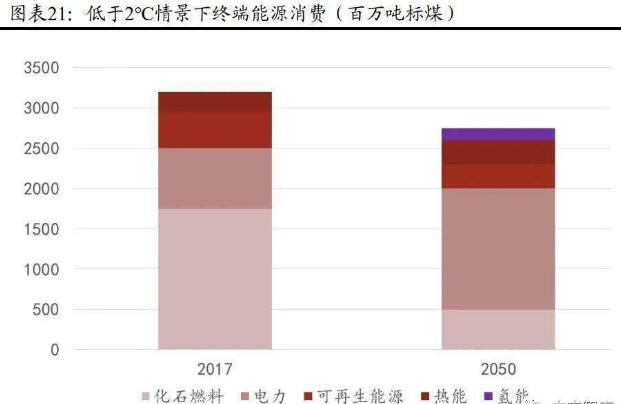

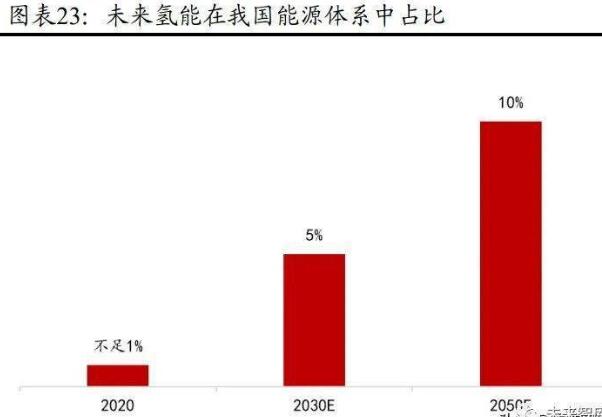

Hydrogen combines development in our country industrial foundation and application of the market. According to the China hydrogen union expects that by 2030, in the hydrogen demand will reach 35 million tons, in terminal energy system accounted for 5%. By 2050 hydrogen will in terminal energy system in China accounted for at least 10%, hydrogen demand close to 60 million tons, 2 oxygen carbon emissions about 700 million tons, industrial output value of about 12 trillion yuan. Among them, with 24.58 million tons of hydrogen transportation field, accounts for about 19% energy-using ratio in this field, equivalent to a reduction of 83.57 million tons of crude oil, or 100 billion cubic meters of natural gas; Industrial field with 33.7 million tons of hydrogen, construction and other fields with hydrogen, 1.1 million tons, equivalent to reduce 170 million tons of standard coal.

2.4 high cost of transporting hydrogen is the primary challenges faced by the hydrogen popularization in China

Hydrogen on a large scale, low cost hydrogen production is to reduce the price of the primary problem solving. According to the energy chain data, the current German hydrogen price of 9.5 euro/kg (about 74.4 yuan/kg), and oil price is $1.53 / liter (or RMB 10.85 yuan/liter). The current hydrogen price $15 / kg (about 106.35 yuan/kg). High prices at the core of the reason is that only 33% of hydrogen is derived from secondary energy, 67% of hydrogen or to be a carbon tax, and oil is the United States is currently $0.77 per litre (5.46 yuan/liter). The current price is RMB 70 yuan/kg of hydrogen. Domestic current hydrogen gas sale price of about 60-70 per kilogram (average, without subsidies), public transport buses run 100 kilometers, the need of about 8 kg, or 480-560 yuan. Contrast using diesel, 100 km of $220, using hydrogen cost remains high. Run about 100 km and ordinary passenger cars need about 1 kg of hydrogen, the corresponding is 60-70 yuan, with regular gasoline vehicles cost.

Hydrogen transport cost is one of the most important aspects of the cost of filling stations in China, also is the key to lower the price of hydrogenation. According to the International Journal of Hydrogen Energy, "the study of cost of filling stations in Shanghai, standing outside the integrity of Hydrogen filling stations and compared for high pressure Hydrogen filling stations, the hydrogenation of lower cost, the main reason is to the Hydrogen filling stations" raw material "industrial truck cost is relatively high, this is also one of hydrogenation in developed countries because of lower price. Because most of China's hydrogenation probably didn't stand the ability of hydrogen, so take advantage of the long tube trailer transport capacity becomes very important. Lowering the cost of transporting hydrogen can compensate for the cost gap with developed countries, reduce the price of hydrogenation.

3 sea rich by diving days fly high as a bird, in the second half of the hydrogen in the industry investment opportunities

3.1 hydrogen fuel cell car sales will explosive growth, 2021, or become the first hydrogen fuel cell development

Affected by the epidemic and policy in 2020, four years in a row growth since 2016, hydrogen fuel cell car is bursting with its first decline in production and sales. The RGL association, according to data from 2020 1199 vehicles, fuel cell car production sales of 1177 units, year-on-year decline 57.5% and 56.8% respectively. Figures show that in February this year, car production and marketing finished 1.503 million and 1.455 million, respectively, from fell by 37.1% and 41.9%, respectively, year-on-year growth of 4.2 times and 3.6 times respectively. Among them, the new energy automobile production finished 124000 and 110000, respectively, year-on-year growth of 7.2 times and 5.8 times respectively, new energy vehicles has for eight months in a row set production and sales history records that month.

As the outbreak dissolved and fuel cell policy demonstration to inform policy in the second half of the year, the national fuel cell car production is expected to have greatly ascend. Before 2020, thanks to sustained fuel cell unclear in subsidy policy, markets wait-and-see attitude is obvious. In the second half of the hydrogen demonstration city officially announced, will promote the local fuel electric pool, with the rapid development of automobile industry chain parts localization of r&d process will get reward policy and so on strong support. And in terms of infrastructure support, is now released under construction around the proposed number of filling stations, 2021 plus hydrogen station number is expected to have new breakthrough, or to reach 150-200, also provide hydrogen fuel cell vehicles with "blood".

The growth potential of hydrogen fuel cell car production and sales data is expected in the second half of the year. Because hydrogen fuel cell industry chain in the first and second quarter with the downstream manufacturers to discuss technical solution, develop business contract, order the goods, in the third quarter purchasing production and confirm the delivery in the fourth quarter. If the policy of "ten city 10 vehicles" in the third quarter to fall to the ground, hydrogen fuel cell car in 2021 has the potential to more than 10000 vehicles. From the point of cars, hydrogen fuel passenger cars and heavy card will occupy 2021 main hydrogen fuel cell car market. This is mainly due to the 2021 China will do must prepare for the 2022 Beijing Olympics, we expect a heavy hydrogen fuel card will begin in the second half of 2021 demonstration operation gradually fall to the ground.

3.2 track broad prospect, the economic value in the links of mining segment

The hydrogen supply side wide space of market, with billions of market potential. The hydrogen supply side including the hydrogen system, storage, shipment. According to the China hydrogen union expects that by 2030, China hydrogen demand will reach 35 million tons, in terminal energy system accounted for 5%. By 2050 hydrogen will in terminal energy system in China accounted for at least 10%, hydrogen demand quantity is close to 60 million tons.

Grey hydrogen high proportion of our country, the future will be replaced by green hydrogen blue hydrogen. According to the national energy information platform, according to research our country current hydrogen production more than 90% of raw material comes from the chemical reforming of traditional energy sources. Of these, 48% come from natural gas reforming, 30% from alcohol reforming, 18% from coke oven gas reforming, only about 4% comes from the electrolysis of water. We expect that with the gradual improvement of the environmental regulation, the future no CCUS technology of hydrogen production fossil fuels (ash) hydrogen will gradually be electrical solutions for water hydrogen hydrogen (green) and combined with carbon CCUS technology of hydrogen production fossil fuels replaced hydrogen (blue).

Green hydrogen estimates:

Our pv wind power installed peak, electrolysis of water hydrogen production prospects. Because the electricity of the total water electrolysis hydrogen production cost of about 80%, so the cost of water electrolysis hydrogen production is the key to energy dissipation problem. On the one hand, by developing a PEM and SOEC technology can reduce the energy consumption in the process of electrolysis, on the other hand depends on the development of photovoltaic (pv) and wind power low cost hydrogen production. When the electricity price is less than 0.50 yuan per KWH, electrolysis of water preparation of hydrogen and gasoline costs. Under the current electricity price, the cost of hydrogen production by electrolysis of water in 20-40 yuan per kg, with China's photovoltaic (pv) and wind power, the gradual expansion of electrolysis of water hydrogen production is expected to reach parity in the future, when the price dropped to 0.1 0.2 yuan per kilowatt, electrolysis of water hydrogen production cost can be decreased from 10-20 yuan per kilogram. According to its Chinese energy research institute, photovoltaic (pv) system in China in 2019 KWH cost about 0.29-0.80 yuan per KWH, to 2025 annual electricity cost in 0.22 0.462 yuan per KWH. Onshore wind KWH cost about 0.315-0.565 yuan per KWH, and falling in the future there is still a certain space, is expected to 2025 annual electricity cost in 0.245 0.512 yuan per KWH. We predict 30/40 / green hydrogen cost 50 years of 21.56/14.46/9.70 yuan per kg respectively.

Blue hydrogen hydrogen aspect:

Our country coal hydrogen production technology mature, has been commercialized and has obvious cost advantages. At present our country coal hydrogen production cost about 0.8 1.2 yuan/square, there is the basis of large-scale hydrogen production, and abundant coal resources in our country, hydrogen production from coal is our country current main ways of hydrogen production. The situation of coal resources in our country mainly is much poor and rich north south east west. Leading in Inner Mongolia, shanxi coal production, coal prices are relatively low. When the coal price is 600 yuan, large-scale coal gasification in the production of hydrogen into this is 1.1 RMB/Nm3. If the area rich in coal resources, coal price reduced to 200 yuan/tons, hydrogen may reduce the cost of RMB 0.34 / N m3. But because the price of coal fell space is limited, and coal gasification has formed large-scale hydrogen production enterprises, the future coal hydrogen production space smaller cost reduction. However, hydrogen production from coal carbon emission problems, although not to CCS is expected to solve the problem of CO2 emissions, but also will increase the cost of hydrogen production. In addition, the fossil fuel hydrogen production technology, production of gas impurity composition, if you want to used in fuel cell need further purification, increase the cost of purification. Carbon neutral, carbon in my countries under the aim of the peak, the application of the CCUS technology will be gradually popularization, we expect the 2030-2040 grey hydrogen will gradually be replaced by the blue hydrogen, we expect with blue hydrogen permeability increase, the 2020-2050 the comprehensive cost of hydrogen production in hydrogen production from fossil fuels will gradually rise to 18.32 yuan per kilogram.

According to the 2019 China hydrogen energy and fuel cell industry white paper on China's hydrogen supply side structure prediction, according to classify the green hydrogen, blue grey hydrogen can draw PingJunZhi hydrogen cost. Together, in the short term because the alternative to grey blue hydrogen hydrogen, hydrogen production cost in 2020-2040 have a certain degree of growth, but as the solar hydrogen production gradually cast production and popularization of the project, 2050 green hydrogen accounted for 80% of the target if can achieve, PingJunZhi hydrogen cost in China is expected to fall to 11.42 yuan per kilogram. Because the industry is still in the import period, hydrogen gas may be affected by the fluctuation of supply and demand, the price of the gross margin was 10%, the hypothesis of the forecast average value of hydrogen. Combining hydrogen demand, we predict that the hydrogen supply end market space 30/40/50 years is expected to reach 761.59 billion yuan / 572.75/5850.38.

Momentum of rapid filling station construction, market space can amount to billions of level. According to our country "energy conservation and new energy vehicle technology road map" for the number of filling stations in planning, is expected to reach 1000 in 2025, is expected to reach 5000 in 2035, the forecast will be built by 2050 or 10000 filling stations. Zhongshang industry research institute, according to data from the hydrogen cost accounts for about 70% of the price plus hydrogen. On the basis of energy saving and new energy vehicle technology roadmap (version 2.0) requirements, is expected to 2050 hydrogenation capacity is expected to reach 4000 kg per day. We suspect that the hydrogen station market space in the 25/35/50 years of 68.26/871.59/264.743 billion yuan respectively.

Hydrogen fuel cell car scale is expected to reduce costs, or will open the trillion-dollar market space. According to our country "energy conservation and new energy automotive technology roadmap" for fuel cell vehicles in general technical route planning, in 2020, plans to realize fuel cell vehicles in certain area small demonstration application in the field of public service vehicles, 5000 scale; In 2025 in the urban areas of private car, public service car achieve high-volume applications, 50000 scale; Private passenger vehicles in 2030, large commercial vehicle to achieve large-scale commercial promotion, reach millions of vehicles. According to the data, combining the current situation of the development of fuel cell car commercial vehicles, passenger cars in our country, we expect 2050 fuel cell vehicles market scale will reach 5 million, assuming that all 10000 2020 for commercial vehicles, 2025 in 50000, 70% for commercial vehicles, 50% for commercial vehicles in 2030 in 1 million, 40% of 5 million vehicles in 2050 for commercial vehicles.

In addition, according to the energy saving and new energy automotive technology roadmap for bike cost planning, we use the bicycle is the most big cost to conservative estimates, the 2020 fuel cell vehicles commercial vehicles, passenger car cost 1.5 million yuan respectively, 500000 yuan; In 2025, 1 million yuan respectively, 300000 yuan; In 2030, 500000 yuan and 200000 yuan respectively, according to the development of technology, we estimate that in 2050 two models cost will fall further, fell to 300000 yuan and 100000 yuan respectively. Based on the above data, we on the bike value estimation, and thus calculate the fuel cell car vehicle market space. Expected 21/25/35/50 fuel cell car space scale will reach 3850/9900 165/869 / one hundred million yuan.